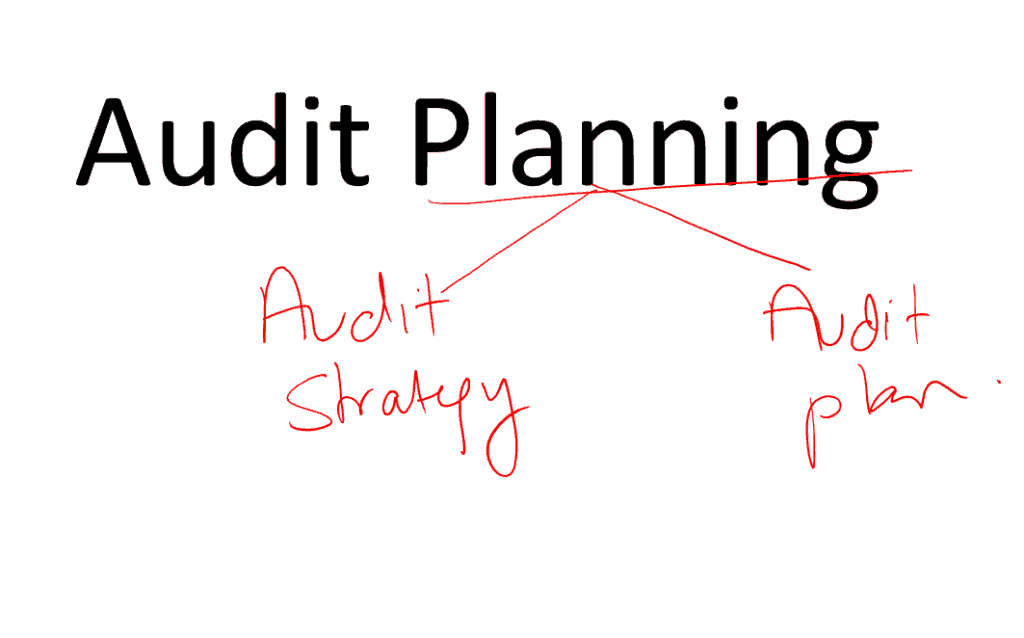

Audit planning

Audit planning ( Audit Strategy and Audit Plan)

Importance of audit planning

- It helps the auditor to devote applicable attention to big areas of the audit.

- It helps the auditor spot and resolves potential issues on a timely basis.

- This helps the auditor to properly organize and manage the audit engagement so it’s performed in an {efficient|a good} and efficient manner.

- It assists within the choice of engagement team members with applicable levels of capabilities and ability to reply to anticipated risks and also the correct assignment of labor to them.

- It facilitates the direction and management of engagement team members and also the review of their work.

- This assists, where applicable, in the coordination of work done by experts

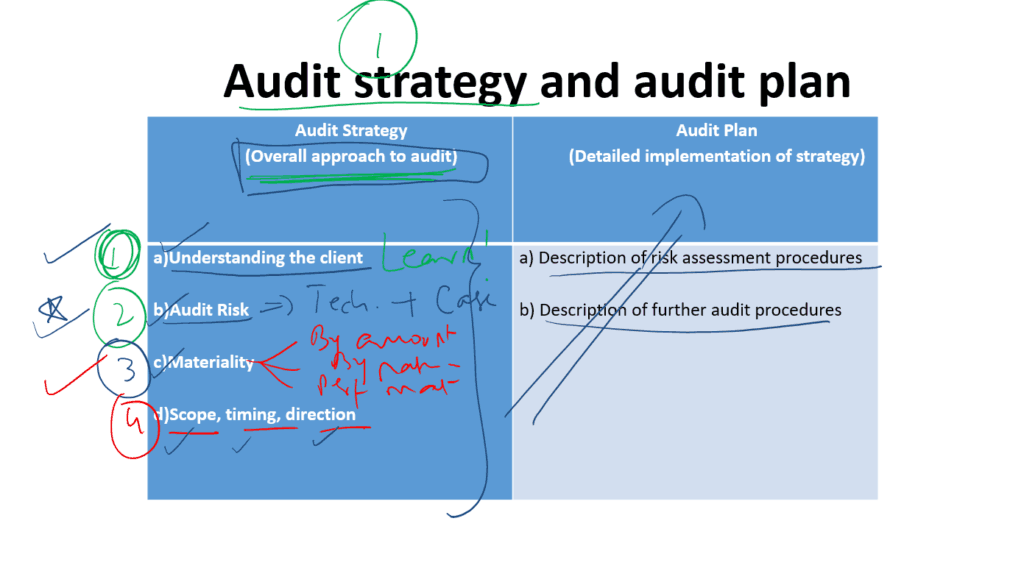

Audit Strategy: Associate in Nursing audit strategy sets the scope, timing, and direction of the audit and guides the development of a more detailed audit plan.

Audit plan: Once the overall strategy has been planned, detailed consideration can be given to each individual audit objective and how it can be best met.

A. UNDERSTANDING THE CLIENT

KNOWLEDGE OF THE BUSINESS / UNDERSTANDING OF THE CLIENT

The auditor obtains an Associate in the Nursing understanding of the entity, its control environment, and its detailed internal controls:

- To identify and assess the risks of material misstatements in the financial statements and to provide a basis for designing and implementing responses to these risks

- To determine the extent to which the auditor would rely on the internal control system.

- To assess whether the team is competent to perform the audit

- To understand relevant laws and regulations impacting the entity

- To consider the reliability of various evidence sources.

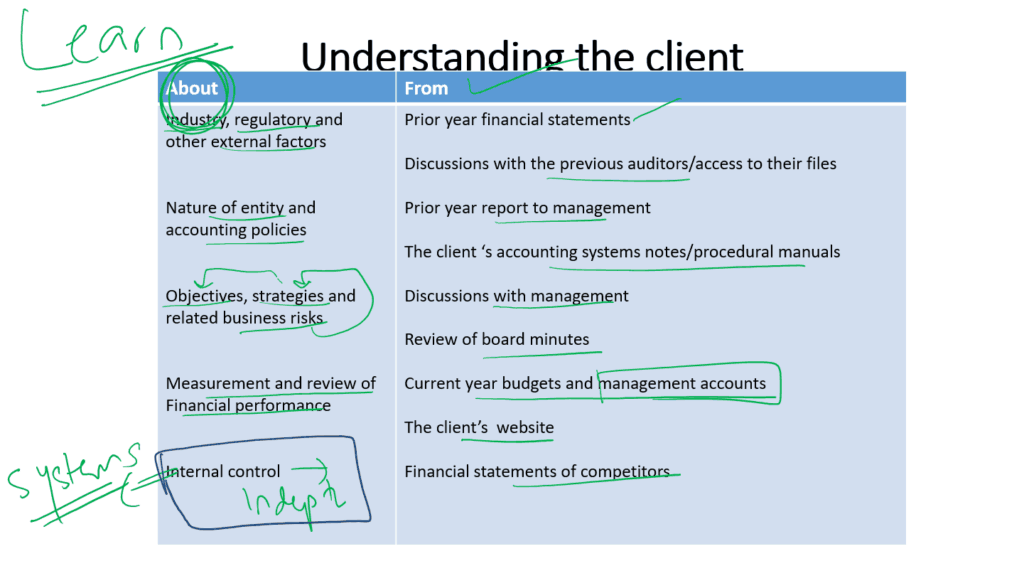

Understanding to be gained about– Industry, regulatory, and other external factors

( for example financial reporting framework, laws and regulations, stakeholders, economic conditions like the volatility of exchange rates, competition, level of technology.

type of entity and accounting policies ( legal structure, ownership, and governance, main sources of finance).

Objectives…strategies…related business risks!– Measurement and review of Financial performance ( measures important to the client, KPIs, budgets, targets).

Internal control (gain an understanding of the design and implementation of internal controls)

other issues that arose in the prior year’s audit and how these were resolved.

Also whether any points brought forward were noted for consideration for this year’s audit.

Internal control deficiencies noted in the prior year;

if these have not been rectified by management then they could arise in the current year audit as well as significant changes in the entity as compared to prior years. Is the company using e-commerce?

Understanding can be gained from the prior year’s financial statements:

- It provides information in relation to the size of the client as well as the key accounting policies, disclosure notes, and whether the audit opinion was modified or not.

- Discussions with the previous auditors/access to their files: Provides data on key problems known throughout the previous year’s audit further because of the audit approach was adopted.

- Previous year report back to management: If this may be obtained from the previous auditors or from management, it can provide information on the internal control deficiencies noted last year. If these haven’t been corrected by management, then they could arise in the current year’s audit as well and may impact the audit approach.

- The client‘s accounting systems notes/procedural manuals: Provides information on how each of the key accounting systems operates and this will be used to identify areas of potential control risk and help determine the audit approach.

- Discussions with management: Provides information in relation to the business, any important issues which have arisen, or changes to accounting policies from the prior year.

- Review of board minutes: Provides an outline of key problems that have arisen throughout the year and the way those charged with governance have self-addressed them.

- Current year budgets and management accounts: Provides relevant financial information for the year to date. It will facilitate the auditor throughout the look stage for preliminary limited review and risk identification.

- The client’s website: Recent press releases from the company may provide background on the business during the year as this will help in identifying the key audit risks.

Important: Risks in companies using E-commerce

- Loss of transaction integrity

- Security risks e.g. virus attacks

- Adoption of improper accounting policies e.g.improper revenue recognition

- Non- compliance with tax and legal requirements

- Failure to ensure that e-commerce contracts are binding in a court of law

- Over-reliance on e-commerce

- Systems and infrastructure crashes

Read More: AUDIT RISK and Auditor Response